The Alabama Center for Real Estate created the following rankings based on average days on market (DOM) for closed transactions during March.

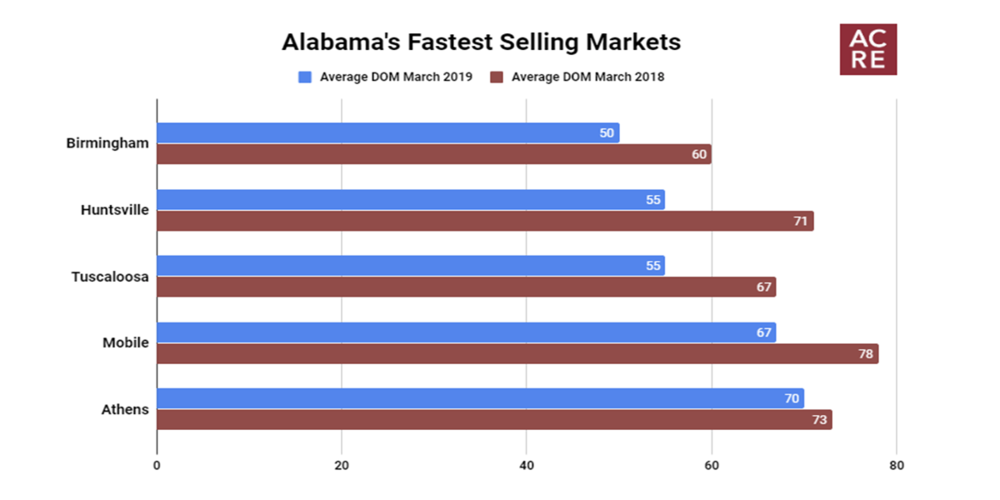

- 1. Birmingham – 50 days

- 2. Huntsville – 55 days

- 2. Tuscaloosa – 55 days

- 4. Mobile – 67 days

- 5. Athens – 70 days

Statewide Average – 99 days

National Average – 65 days

Birmingham– Birmingham was Alabama’s fastest selling market in March with a DOM average of 50 days. Birmingham was also Alabama’s fastest selling market during 2018 with an annual DOM average of 52 days. March 2019 days on market improved 17 percent from March 2018’s DOM of 60 days. Surprisingly, total residential sales in the area decreased 4.0 percent year-over-year (y/y). However, median sales price rose 12.6 percent y/y and average sales price rose 10.3 percent y/y. Mirroring statewide trends, residential listings in the Birmingham area decreased 7.6 percent from one year ago. The Birmingham area also saw a 2 percent decrease y/y in their average number of listings during the first quarter. Lastly, Birmingham is still a seller’s market as months of supply decreased from 3.8 one year ago to 3.7 during March.

Huntsville– With a days on market (DOM) average of 55 days, Huntsville was tied for second for Alabama’s fastest selling market during March. Huntsville was Alabama’s second fastest selling market in 2018 with an annual DOM average of 57 days, second to Birmingham with 52. Compared to March 2018, Huntsville experienced a 22.5 percent improvement in average DOM, decreasing from 71 days to the current 55. Months of supply also saw a considerable decrease, dropping from 2.7 months to 2.0 months, tying Athens for the strongest seller’s market in the state in March. Going forward, expect properties in the area to continue to sell at a fast pace as tightening inventory trends from 2018 have continued into March. Listings in the area declined 34.5 percent year-over-year (y/y) from 1,767 in March 2018 to 1,157 currently. It is possible, however, that an increase in finished lot inventory in the Huntsville area will provide some inventory relief as this creates an opportunity for the already strong new construction market to expand to new heights.

Tuscaloosa– With a DOM average of 55 days, the Tuscaloosa area tied for Alabama’s second fastest selling market in March with the Huntsville area. The Tuscaloosa area’s DOM improved 17.9 percent y/y, dropping from 67 to 55 days. Closed sales in March increased 0.4 percent y/y, sustaining the record sales pace set in 2018. Mirroring statewide trends but to a lesser degree, residential listings in the Tuscaloosa area dropped 3.1 percent y/y, from 859 listings one year ago to 832 currently. March’s inventory of 832 units is also over 30% below the 5-year inventory average of 1,199 units. With increasing sales and tightening inventory, it is not surprising to see months of supply in the Tuscaloosa area trending downwards. The area currently has 3.4 months of supply, reflecting a seller’s market in the area.

Mobile– Residential properties selling in March averaged 67 days on the market, making the Mobile area Alabama’s fourth fastest selling market in March 2019. Residential sales in the area increased 10.2 percent from 381 closed transactions in March 2018 to 420 currently. The area’s median sales price also increased 7.2 percent from $138,915 to $148,950. Average days on market improved by 11 days, or 14.1 percent, from one year ago. Mirroring statewide trends, residential properties for sale during March declined 12.2 percent from one year ago. The Mobile area currently has 3.3 months of supply, reflecting a seller’s market in the area. With another strong month in real estate, the region has a bright outlook for 2019 and beyond as the Port of Mobile continues to diversify its operations to accommodate the state’s changing economy.

Athens– The Athens area was Alabama’s fifth fastest selling market in March with a DOM average of 70 days. Total residential sales increased 16.1 percent from March 2019. Almost 40 percent of all residential sales were new construction properties, continuing the trend of Athens having the highest percentage in the state in this category (new construction as a percentage of total residential sales). The Athens area saw DOM improve 4.1 percent from 73 days last year to 70 currently. Mirroring regional trends, total units listed for sale declined 26.1 percent y/y from 460 units one year ago to 340 in March. With strong sales growth and tightening inventory, it is not surprising to see the area’s months of supply trending downwards. Athens had 2.0 months of supply in March, reflecting a strong seller’s market in the area. Nearby Huntsville also had 2.0 months of supply in March, tied for the lowest in the state. Athens and the greater Huntsville metro area are both poised for sustained growth as the regional economy continues to attract technology and manufacturing companies. Additionally, the outlook for 2019 and beyond is strong as the $1.6 billion Mazda Toyota facility broke ground in late 2018, with automobile production beginning in 2021.