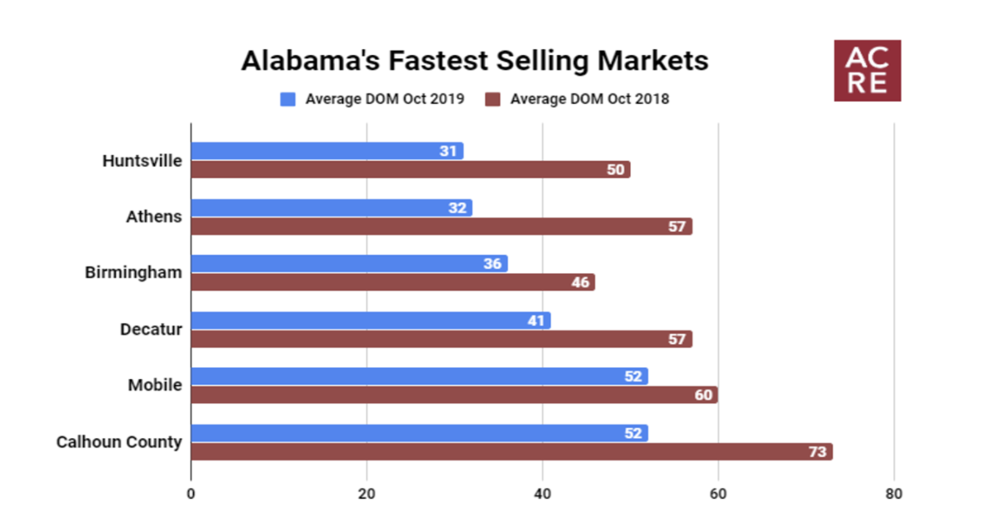

The Alabama Center for Real Estate created the following rankings based on average days on market (DOM) for closed transactions during October.

- 1. Huntsville: 31 days

- 2. Athens: 32 days

- 3. Birmingham: 36 days

- 4. Decatur: 41 days

- 5. (Tie) Mobile and Calhoun County: 52 days

Statewide Average: 88 days

National Average: 66 days

Huntsville– With an average DOM of 34 days, the Huntsville area was Alabama’s fastest selling market in October. The area now has 38 consecutive months of Y/Y improvement in average DOM, an impressive streak that began in October 2016. The area’s YTD DOM average improved from 59 in 2018 to 44 in 2019, making it the second fastest selling market in the state YTD behind Birmingham. Mirroring statewide trends but to a greater degree, residential listings in the Huntsville metro area during October were down 27% from one year ago. Demand for housing was especially strong as sales increased 15.5% Y/Y from 612 to 707 closed transactions. While the area has, arguably, the tightest inventory in the state, and continued sales growth (up 5.4% YTD), it was not surprising to see home price appreciation in the area continue to trend upwards. Huntsville’s median sales price increased 17.5% Y/Y during October, ahead of the statewide average of 10.1%. Dollar volume is rising fast as it increased 23.4% Y/Y from $143 million in October 2018 to $176 million in October 2019.

Athens– Driven in part by a strong new construction market, Athens was Alabama’s second fastest selling market in October with a DOM average of 32 days. Properties sold in October closed 25 days faster than one year ago, while the area’s year-to-date DOM average improved from 62 in 2018 to 50 in 2019. Average DOM in the Athens area has improved Y/Y for 24 consecutive months, a streak that began in November 2017. Mirroring trends seen across the north Alabama region, inventory declined 31% Y/Y, extending the streak of Y/Y inventory declines to 51 months. While the total number of closed transactions decreased 7.4% Y/Y in October, sales are up 8.2% YTD. With tight inventory and growing demand for housing in the area, it was surprising to see the area’s median sales price fall 4.2% Y/Y. Year-to-date, however, the area has the fourth fastest home price appreciation in Alabama’s metro areas (8.8%). Dollar volume declined 5.8% from $35.3 million one year ago to $33.3 million during October, ending the area’s streak of 46 months of dollar volume gains.

Birmingham– With an average DOM of 36 days, the Birmingham area was Alabama’s third fastest selling market in October. Residential markets in the area now have 35 consecutive months of Y/Y improvement in average DOM, a streak that goes back to December 2016. Mirroring statewide trends but to a lesser degree, inventory was tight during October as listings declined 6.1% from one year ago. Inventory shortages in Alabama’s largest residential market, however, are quite different from the second largest market, the Huntsville area. Inventory declines of 25-30% are the new normal in the Huntsville area and larger north Alabama region. On the demand side, total residential sales in the Birmingham area increased 2.6% Y/Y, building upon the growth seen in 2018, a record year for residential sales activity in the state. After a strong October, sales are now up 3.1% YTD. Home price appreciation regained momentum as the median sales price in the Birmingham area increased 5.1% Y/Y, and the market is now up 5.5% YTD. With 4.0 months of supply, Birmingham is a seller’s market, a factor contributing to rising home prices. Dollar volume is on the rise as it increased 8.6% in October from $296 million one year ago to $322 million currently.

Decatur– Residential properties in this area sold at an average of 41 days, down 16 days Y/Y and 15 days YTD when compared to October of last year. Following statewide trends, Decatur saw a significant drop in inventory this month, falling 21.2% Y/Y, continuing the 56 month streak dating back to January 2015. Total residential sales saw a nice boost this month of 11.5% Y/Y, bringing year-to-date sales growth to 1.1%. Dollar volume in this area increased 29.6% from $19.7 million in October of last year to $25.5 million currently.

Mobile– Residential properties sold in October averaged 52 days on the market, tying the Mobile area for fifth. This represents an improvement of 8 days from one year ago. Year-to-date, properties in the area are selling 13 days faster than this time last year. Mirroring statewide trends, inventory is also short in the area as listings declined 12.4% Y/Y, extending the area’s streak of inventory declines to 72 months, the longest in the state. Total residential sales increased significantly (13.7%) in October, and the market is up 4.7% YTD. Home price appreciation was strong in October, increasing 2.8% Y/Y. It is now up 4.5% on the year (YTD), just behind the statewide average of 5.5%. Dollar volume increased 16.8% Y/Y from $60 million in October 2018 to $70.1 million in October 2019.

Calhoun County– Alabama’s fifth fastest selling market (tie with Mobile) averaged 52 days on the market during October, an improvement of 19 days from one year ago. Year-to-date, properties in the area are selling nine days faster than in 2018. Total listings in the area declined 9.3% in October, extending the area’s streak of Y/Y inventory declines to 14 months. Of Alabama’s 14 metro areas*, only one experienced an inventory gain in October (Lee County up 9.5% from October 2019). On the demand side, sales declined in October, falling 17.1% Y/Y, but they are up 4.1% YTD. The area’s median sales price decreased 6.0% from $146,250 to $137,450, while the YTD median sales price is up 1.0% from last year. Dollar volume also fell this month as it decreased 14.4% from $25.5 million one year ago to $21.8 million currently.